For centuries, the insurance industry has relied on human judgment, statistical averages, and historical patterns to evaluate risk. Actuaries calculated probabilities using large datasets, underwriters assessed individual cases, and insurers set premiums based on broad categories such as age, location, or occupation. While these traditional methods created a functional system for managing uncertainty, they often lacked precision and adaptability.

Today, a quiet revolution is reshaping this process. Algorithms powered by artificial intelligence (AI), machine learning, and advanced analytics are transforming how insurers evaluate risk, price policies, and interact with customers. This technological shift is not simply improving efficiency—it is fundamentally changing the nature of insurance itself.

The result is a new era in which risk is increasingly measured, predicted, and priced by intelligent systems capable of analyzing vast amounts of data in real time.

From Historical Data to Real-Time Intelligence

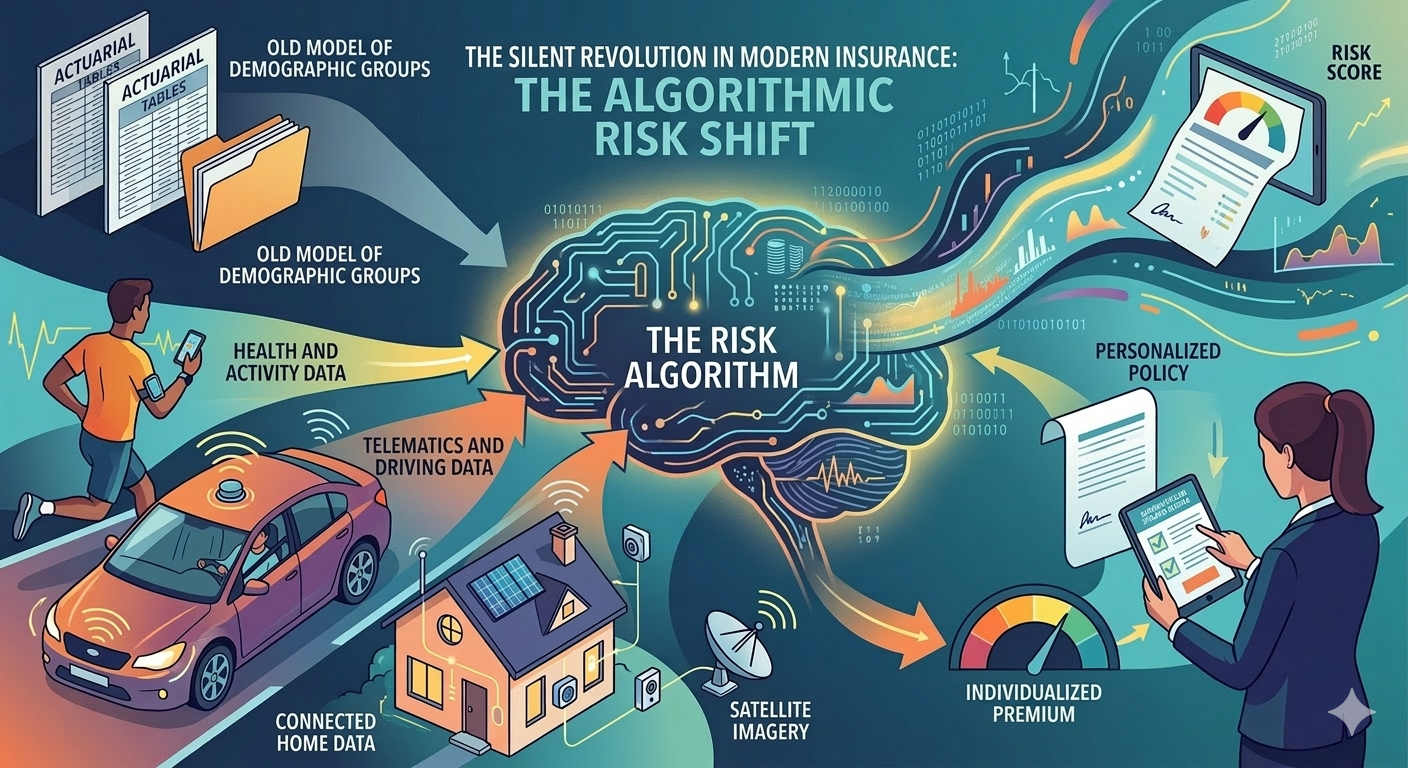

Traditional insurance models relied heavily on historical data. Insurers examined past claims, demographic statistics, and regional trends to estimate the likelihood of future events. While this approach provided useful insights, it often generalized risk across large groups rather than individuals.

Modern algorithms, however, allow insurers to move beyond broad averages. AI systems can process enormous datasets containing behavioral, environmental, and economic information. These datasets may include telematics from vehicles, health metrics from wearable devices, satellite imagery for climate risk analysis, and real-time financial indicators.

By analyzing these diverse inputs, algorithms can detect subtle correlations that traditional statistical models might overlook. Instead of simply categorizing policyholders into general risk groups, insurers can now estimate risk with far greater precision.

This shift from historical averages to real-time intelligence enables more dynamic and personalized insurance models.

The Rise of Personalized Risk Pricing

One of the most significant consequences of algorithmic underwriting is the emergence of personalized pricing. Rather than assigning premiums based solely on demographic categories, insurers can now evaluate the behavior and characteristics of individual policyholders.

For example, usage-based auto insurance programs collect driving data through telematics devices or smartphone applications. These systems monitor factors such as speed, braking patterns, driving time, and mileage. Drivers who demonstrate safer habits may receive lower premiums, while riskier behavior may lead to higher rates.

Similarly, health insurance providers increasingly incorporate wearable technology data to encourage healthier lifestyles. Activity levels, heart rate patterns, and sleep metrics can help insurers assess health risks more accurately while also promoting preventive care.

This individualized approach benefits responsible customers by rewarding lower-risk behavior. At the same time, it allows insurers to reduce uncertainty and price coverage more precisely.

Artificial Intelligence and Predictive Risk Modeling

Artificial intelligence is particularly powerful in predictive modeling. Machine learning algorithms can analyze enormous volumes of historical and real-time data to identify patterns that indicate future risk events.

In property insurance, AI models can evaluate climate patterns, urban development trends, and geographic data to predict the likelihood of floods, wildfires, or severe storms. Insurers can use these predictions to adjust premiums, design new coverage products, or implement preventive measures.

Similarly, AI can detect emerging risk patterns in financial or business insurance. Corporate insurers may analyze economic indicators, supply chain data, and geopolitical developments to estimate potential disruptions affecting insured companies.

These predictive capabilities allow insurers to move from reactive systems—paying claims after losses occur—to proactive risk management strategies aimed at preventing losses in the first place.

Fraud Detection and Operational Efficiency

Another major advantage of algorithmic systems is their ability to detect fraudulent claims. Insurance fraud has long been a costly problem for the industry, increasing operational expenses and ultimately raising premiums for honest policyholders.

AI-powered fraud detection tools can analyze claims data, transaction histories, and behavioral patterns to identify suspicious activity. These systems compare new claims against millions of previous cases, flagging anomalies that may indicate fraud.

For example, algorithms can identify unusual claim frequencies, inconsistencies in documentation, or patterns linking multiple claims to the same network of individuals.

In addition to fraud detection, automation significantly improves operational efficiency. Claims processing, policy underwriting, and customer support can now be partially automated using intelligent systems. Tasks that once required days or weeks can often be completed in minutes.

This efficiency reduces administrative costs and improves customer experience by accelerating claims resolution.

Ethical Challenges and Data Privacy

Despite the advantages of algorithmic insurance models, their rapid adoption raises important ethical and regulatory questions.

One major concern involves data privacy. Personalized risk assessment requires access to sensitive personal information, including health data, behavioral metrics, and location tracking. Insurers must ensure that this data is securely stored and used responsibly.

Another challenge relates to algorithmic transparency. Machine learning models can be highly complex, sometimes functioning as “black boxes” whose decision-making processes are difficult to interpret. Policyholders may question how premiums are determined if the logic behind pricing algorithms is not clearly explained.

There is also the risk of unintended bias. If training data contains historical inequalities or skewed patterns, algorithms may reproduce those biases in pricing decisions. Regulators and insurers must work together to ensure fairness and accountability in automated systems.

Regulation in an Algorithmic Insurance Market

Regulatory frameworks for insurance are evolving to address these challenges. Governments and financial authorities increasingly require transparency in algorithmic decision-making, particularly when automated systems affect consumer pricing or eligibility.

Some regulators are also exploring guidelines for ethical AI usage, ensuring that algorithms operate within fair and accountable standards.

Balancing innovation with consumer protection will be critical as algorithmic underwriting becomes more widespread.

A Hybrid Future: Humans and Algorithms

Although algorithms are becoming central to risk assessment, the future of insurance will likely involve a hybrid model combining technology with human expertise.

AI systems excel at processing data and identifying statistical patterns, but human professionals remain essential for interpreting complex situations, resolving disputes, and designing strategic insurance products.

Underwriters, actuaries, and risk analysts will increasingly collaborate with intelligent systems rather than being replaced by them. The human role will shift toward oversight, strategic decision-making, and ethical governance of algorithmic tools.

The Transformation of Risk Management

The integration of algorithms into insurance pricing represents more than a technological upgrade—it marks a structural transformation in how societies manage uncertainty.

Insurance has always been about predicting risk and distributing financial protection across communities. By harnessing the analytical power of artificial intelligence, insurers can now measure risk with unprecedented accuracy and responsiveness.

However, this transformation also raises important questions about privacy, fairness, and the future balance between automation and human judgment.

Conclusion

The silent revolution unfolding in the insurance industry is driven by algorithms capable of analyzing complex data at extraordinary speed and scale. These intelligent systems are redefining risk assessment, enabling personalized pricing, improving fraud detection, and transforming how insurers operate.

Yet the success of algorithmic insurance will depend not only on technological innovation but also on responsible governance. Ensuring transparency, protecting data privacy, and maintaining fairness will be essential as insurers adopt increasingly sophisticated models.

Ultimately, the future of insurance will not be controlled solely by algorithms or human experts, but by the collaboration between them—combining technological precision with human insight to build a more resilient and adaptive system of protection in an uncertain world.