Economics often triggers rejection in many people. It is associated with complicated charts, technical language, and difficult concepts. However, economics is not something distant or exclusive to experts: it is present in every daily decision, from buying at the supermarket to saving, taking on debt, or planning for the future.

Understanding the “real economy” doesn’t mean memorizing complex theories; it means understanding how money, prices, employment, and consumption function in daily life. When economics is explained without technicalities, it becomes a powerful tool for making better decisions.

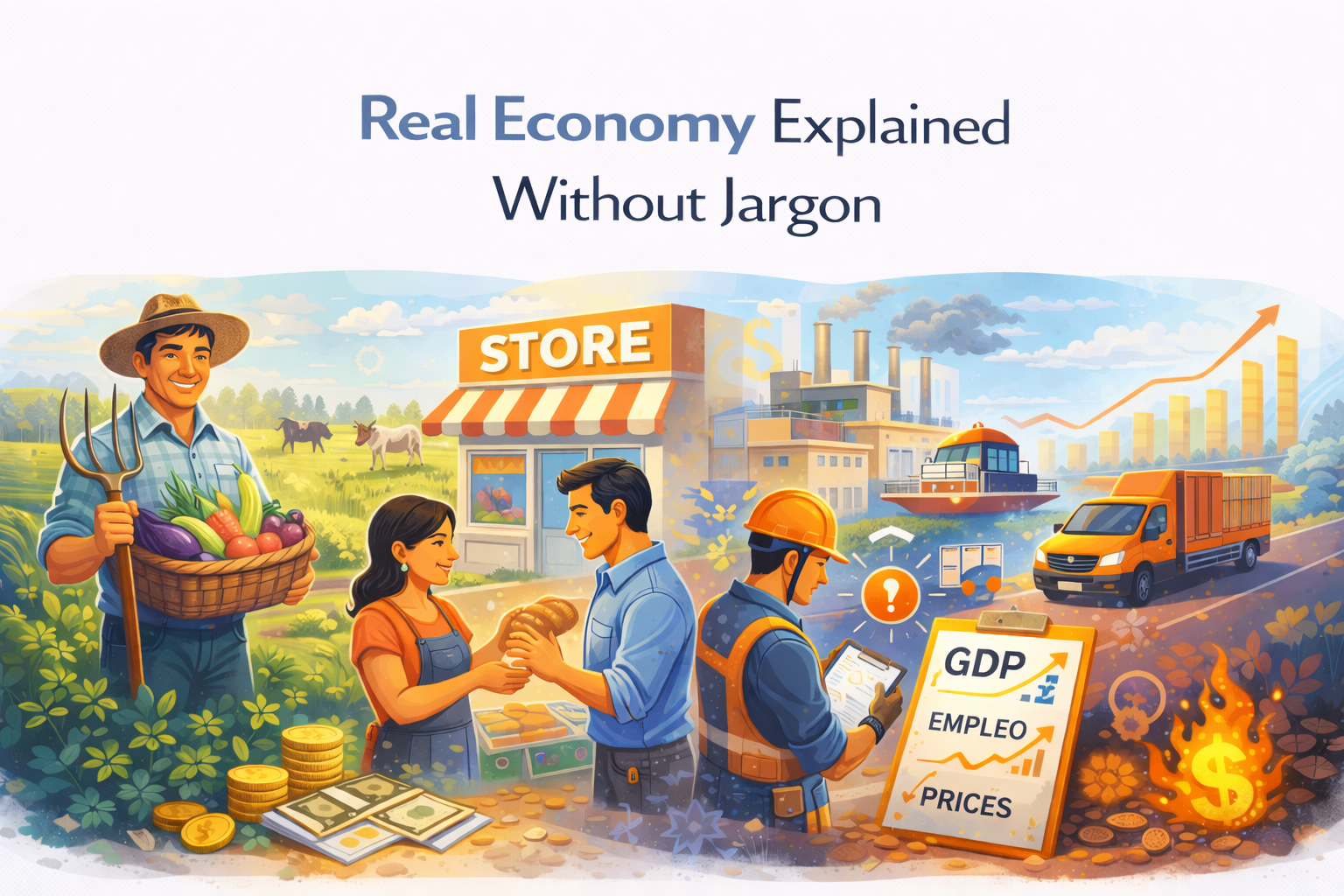

What Economics Really Is

In its simplest form, economics studies how individuals and societies manage limited resources to satisfy unlimited needs. In other words, it’s about deciding what to do with available money, time, and resources. It’s not just about big figures or government decisions. Economics starts at home: when you decide to spend, save, or invest, you are actively participating in the economic system.

The Psychology of Choice and Opportunity Cost

To truly master the real economy, one must grasp the concept of Opportunity Cost. Every time you choose to spend $50 on a dinner out, the real “cost” isn’t just the money—it’s what you didn’t do with that money, such as investing it or putting it toward a future goal. In the real economy, we are constantly making trade-offs.

This leads us to Behavioral Economics, which reveals that humans are not always rational “calculators.” We are influenced by emotions, social pressure, and cognitive biases. For example, we tend to value immediate rewards more than future ones (Present Bias). Understanding that our brains are “wired” to prefer spending over saving is the first step toward hacking our own behavior. By recognizing these mental traps, we can move from reactive spending to intentional resource management, which is the cornerstone of true financial freedom.

Supply and Demand Explained Simply

One of the most important concepts is the relationship between supply and demand.

- Supply: The amount of a product or service available.

- Demand: The number of people who want that product. When something is in high demand but low supply, the price goes up. When there is plenty of supply but little demand, the price drops. This principle explains why certain products become more expensive during specific seasons.

Why Prices Rise (Inflation)

The general increase in prices, known as inflation, reduces purchasing power: with the same amount of money, you can buy fewer things. Causes include:

- Increased production costs.

- Demand exceeding supply.

- Excessive money printing.

- Supply chain issues.

The Shift Toward a Circular and Digital Economy

The real economy of 2026 is no longer just a linear path of “buy, use, and discard.” We are witnessing the rise of the Circular Economy, where value is maintained by repairing, reusing, and recycling. From a personal finance perspective, this shift changes how we perceive “value.” Buying higher-quality goods that last longer—or participating in the “sharing economy” (like car-sharing or tool libraries)—is becoming a sophisticated economic strategy to reduce long-term costs.

Furthermore, the Digital Labor Economy has redefined employment. With the “Gig Economy” and remote work, many people no longer have a single source of income but a “portfolio of skills.” This requires a new type of economic resilience: managing yourself as a micro-business. In this environment, your Human Capital (your knowledge and adaptability) is your most valuable asset. The real economy today rewards those who treat their time as a scalable resource and understand that in a digital world, attention is a currency as valuable as gold.

Credit, Debt, and Government Impact

Credit is not inherently negative; it is a tool. However, the real economy teaches us that every debt has a future cost. Before borrowing, it is vital to analyze repayment capacity. Likewise, government policies—taxes, public spending, and regulations—directly affect your wallet. Even if these decisions are made at a macro level, their effects are felt at the dinner table.

Conclusion: Economics is for Everyone

Real economics is not complicated when explained clearly. It is part of daily life and affects everyone. Understanding it without technicalities allows you to lose the fear, gain confidence, and make better financial decisions. In an increasingly complex world, basic economic knowledge becomes a key advantage for achieving stability and well-being.